Page 26 - WEF Reoprt 2020

P. 26

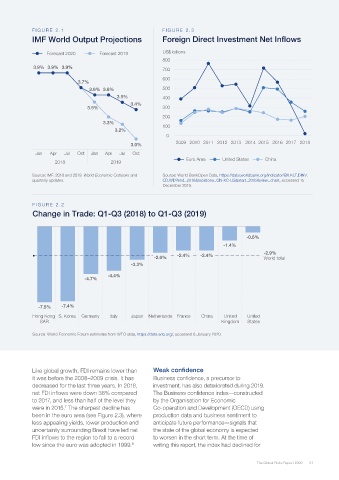

FIG U RE 2 .1 FIG U RE 2 .3

IMF World Output Projections Foreign Direct Investment Net Inflows

Forecast 2020 Forecast 2019 US$ billions

800

3.9% 3.9% 3.9% 700

600

3.7%

3.6% 3.6% 500

3.5% 400

3.4%

3.5% 300

200

3.3% 100

3.2%

0

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

3.0%

Jan Apr Jul Oct Jan Apr Jul Oct

Euro Area United States China

2018 2019

Source: IMF. 2018 and 2019. World Economic Outlooks and Source: World BankOpen Data, https://data.worldbank.org/indicator/BX.KLT.DINV.

quarterly updates. CD.WD?end=2018&locations=CN-XC-US&start=2009&view=chart, accessed 15

December 2019.

FIG U RE 2 .2

Change in Trade: Q1-Q3 (2018) to Q1-Q3 (2019)

-0.6%

-1.4%

-2.9%

-2.4% -2.4%

-2.6% World total

-3.3%

-4.4%

-4.7%

-7.5% -7.4%

Hong Kong S. Korea Germany Italy Japan Netherlands France China United United

SAR Kingdom States

Source: World Economic Forum estimates from WTO data, https://data.wto.org/, accessed 8 January 2020.

Like global growth, FDI remains lower than Weak confidence

it was before the 2008–2009 crisis. It has Business confidence, a precursor to

decreased for the last three years. In 2018, investment, has also deteriorated during 2019.

net FDI inflows were down 38% compared The Business confidence index—constructed

to 2017, and less than half of the level they by the Organisation for Economic

were in 2015. The sharpest decline has Co-operation and Development (OECD) using

7

been in the euro area (see Figure 2.3), where production data and business sentiment to

less appealing yields, lower production and anticipate future performance—signals that

uncertainty surrounding Brexit have led net the state of the global economy is expected

FDI inflows to the region to fall to a record to worsen in the short term. At the time of

low since the euro was adopted in 1999. writing this report, the index had declined for

8

The Global Risks Report 2020 21